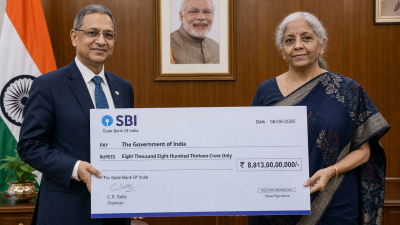

State Bank of India presented a dividend cheque of ₹8,813 crore to the Central government for FY26 after declaring a dividend of ₹17.35 per share. SBI reported net profit of ₹80,032 crore for FY26 (up 12.88%). RBI paid a record ₹2.87 lakh crore to the government; overall PSU dividends for FY26 exceeded budget estimates.

What is the immediate issue

Public sector banks and other public sector enterprises have delivered larger-than-expected dividend flows to the Union government. SBI’s payment and recent ex-dividend dates for several PSBs signal material non‑tax receipts for the Centre in the near term.

Why this matters for governance and the fiscal position

- Fiscal support: Dividend receipts form part of non‑tax revenue and reduce the fiscal gap without increasing taxes or borrowing.

- Policy balance: Government ownership creates a dual role — shareholder seeking returns and regulator/owner pursuing socio‑economic objectives.

- Bank health indicator: Higher dividends reflect improved profitability, asset quality and capital adequacy trends in PSBs, with implications for credit availability and financial stability.

Drivers of higher PSB profitability and dividend capacity

- Improved earnings: SBI’s ₹80,032 crore net profit in FY26 (12.88% y-o-y) raised distributable surplus and supported the ₹8,813 crore dividend to the Centre.

- Asset quality recovery: Lower fresh slippages, recoveries under the Insolvency and Bankruptcy Code and focused resolution improved net interest margins and reduced provisioning burdens.

- Credit growth: Economic revival lifted loan demand, increasing interest income and fee income.

- Cost and operating efficiency: Digitalisation, branch rationalisation and rationalised staff costs improved cost-to-income ratios for several PSBs.

- Reforms and recapitalisation: Prior consolidation, governance reforms and episodic capital support enhanced balance sheet resilience.

Mechanics of dividend declaration and constraints

- Corporate process: Dividend is proposed by the bank board and approved at the shareholders’ meeting; per Companies Act and bank governance norms.

- Regulatory prudence: Dividend distribution is constrained by capital adequacy requirements (Basel III), supervisory expectations from the Reserve Bank and the need to maintain buffers against future shocks.

- Timing and receipt: Ex‑dividend dates determine entitlement; several PSBs had ex‑dividend dates in June 2026 (Bank of Baroda, Indian Bank, Canara Bank, Punjab National Bank), indicating further receipts for the government.

Challenges in sustaining profitability and consistent dividend flows

| Challenge | Implication |

|---|---|

| Competition from private banks and NBFCs | Pressure on margins and market share |

| Capital requirements | High dividends reduce retained earnings; may necessitate fresh capital raising |

| Asset quality risks | Macro shocks can reverse recent NPA improvements and require provisioning |

| Operational and technological gaps | Cost escalation and service delivery risks if upgrades lag |

| Policy mandates | Priority sector lending and social objectives can lower commercial returns |

Measures to strengthen PSB efficiency and dividend sustainability

- Governance reforms: Strengthen board independence, meritocratic senior appointments, and clear performance metrics.

- Capital planning: Balance dividend policy with internal capital generation; use market capital raising when appropriate to avoid undercapitalisation.

- Risk frameworks: Improve credit underwriting, early warning systems and stress testing for macro scenarios.

- Technology and product diversification: Invest in digital platforms, expand fee‑based services and capitalise on Treasury and retail franchises.

- Consolidation and scale: Where needed, pursue strategic mergers to achieve cost synergies and wider footprints.

Government ownership: autonomy, objectives, conflicts and synergies

The Centre holds about 55% equity in SBI. That ownership permits direction and dividend realisation. Ownership effects:

- Synergies: PSBs execute government schemes, widen financial inclusion and deploy counter‑cyclical credit as a public policy tool.

- Conflict areas: Pressure to pay dividends can conflict with the need to retain capital for loan growth or provisioning. Political or social priorities may limit commercial decision‑making.

- Autonomy: Boards and management retain day‑to‑day control, but major strategic moves can be influenced by shareholder (government) expectations.

Dividends as an instrument of resource mobilisation: benefits and limits

- Immediate fiscal benefits: RBI’s record payout of ₹2.87 lakh crore and PSU dividends (government share ₹89,501 crore from 55 listed PSUs) provided a significant non‑tax revenue boost in FY26; total PSU dividends reached ₹78,438 crore (INR 784.38 billion), exceeding revised estimates.

- Short‑term versus structural revenue: Dividend receipts are volatile and depend on annual profits and economic cycles. They are less reliable than structural tax reforms or sustainable revenue sources.

- Reinvestment trade‑off: Large payouts reduce retained earnings and can constrain PSUs’/banks’ capacity for capex, technological investment and lending expansion unless compensated by fresh capital markets or government recapitalisation.

- Fiscal management implication: Using dividends to meet fiscal targets can work in the short run but requires caution in medium‑term fiscal planning to avoid dependence on cyclical corporate profits.

Policy implications and operational recommendations for the Centre

- Balanced dividend policy: Encourage banks to adopt dividend policies that balance shareholder returns with capital retention for growth and resilience.

- Transparent expectations: Publish a clear fiscal framework that treats dividend receipts as cyclical and avoids over‑dependence in budget forecasts.

- Support market solutions: Facilitate well‑timed market capital raising, where needed, rather than recurring recapitalisation by the government.

- Strengthen supervision: RBI surveillance should continue to ensure that dividend payouts do not impair systemic stability or capital adequacy.

Model Questions

- Analyse the significance of dividend receipts from public sector banks and public sector undertakings for the Union government's non‑tax revenue. Assess the sustainability of relying on such receipts for fiscal consolidation. [GS-III: Economic Development] Answer Hint: Define

- dividend receipts and quantify recent flows (RBI ₹2.87 lakh crore; PSU dividends ₹78,438 crore; SBI ₹8,813 crore). Explain short‑term fiscal relief and volatility risk. Assess sustainability: cyclical nature, impact on retained earnings/capital, need for market capital or structural revenue reforms, and prudent fiscal forecasting. Examine the main challenges public sector banks face in sustaining profitability and regular dividend payouts. Suggest institutional and operational measures to address these challenges. [GS-III: Economic Development] Answer Hint: List

- challenges—competition, capital needs, asset quality, technological gaps, policy mandates. Recommend measures—stronger governance, capital planning, improved risk frameworks, digital investment, revenue diversification, selective consolidation and performance‑linked HR reforms to sustain profits and dividends. To what extent does government ownership influence the operational autonomy and policy objectives of public sector banks? Discuss conflicts and synergies between the government's shareholder role and socio‑economic goals. [GS-II: Governance] Answer Hint: Explain

- ownership (e.g., Centre ~55% in SBI), board and management roles, and dual mandate—commercial returns vs social policy. Outline synergies (scheme implementation, inclusion) and conflicts (dividend pressure vs capital needs, political interference). Suggest governance safeguards and clarity of mandates to balance roles. Critically evaluate the implications of the government's reliance on dividend receipts from the Reserve Bank and public sector enterprises for resource mobilisation and fiscal management. [GS-III: Economic Development] Answer Hint: Describe fiscal benefit and examples (RBI and PSU payouts). Evaluate risks—reliance on volatile corporate profits, constraint on reinvestment and bank/PSU capital, possibility of procyclical fiscal policy. Recommend safeguards: conservative budgeting, contingency buffers and promoting sustainable revenue measures.