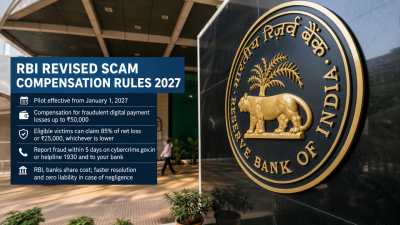

RBI amended its 2017 circular to introduce a one‑year pilot compensation framework for victims of fraudulent electronic banking transactions (EBTs), effective 1 January 2027.

Scope and definition

- Fraudulent EBTs: Transactions executed using stolen credentials or those made under deception or coercion; expands protection beyond unauthorised transactions.

- Who is covered: Individual customers and sole proprietors.

- Loss ceiling: Compensation applies for net losses up to ₹50,000 per incident.

Compensation mechanics

- Amount: Eligible victims may receive 85% of the net loss or ₹25,000, whichever is lower; entitlement available once in a customer’s lifetime.

- Cost sharing: RBI bears about 75% of the compensation cost; for domestic claims capped at ₹25,000 RBI contribution is ₹19,118, while the remitter and beneficiary banks contribute ₹2,941 each.

Reporting & timelines

- Time limit to report: Victim must notify the National Cyber Crime Reporting Portal or Helpline 1930 and the bank within five calendar days of the incident.

- Settlement timelines: Banks to conclude domestic investigations and communicate outcomes within 45 calendar days; cross‑border cases within 60 days.

Bank obligations & dispute handling

- Zero liability: Applies if fraud arises from bank negligence or a third‑party breach reported within five days.

- Credit‑card disputes: Banks must issue a “shadow reversal” (temporary credit) within five days of complaint.

- Pilot status: Framework effective 1 Jan 2027 for one year.